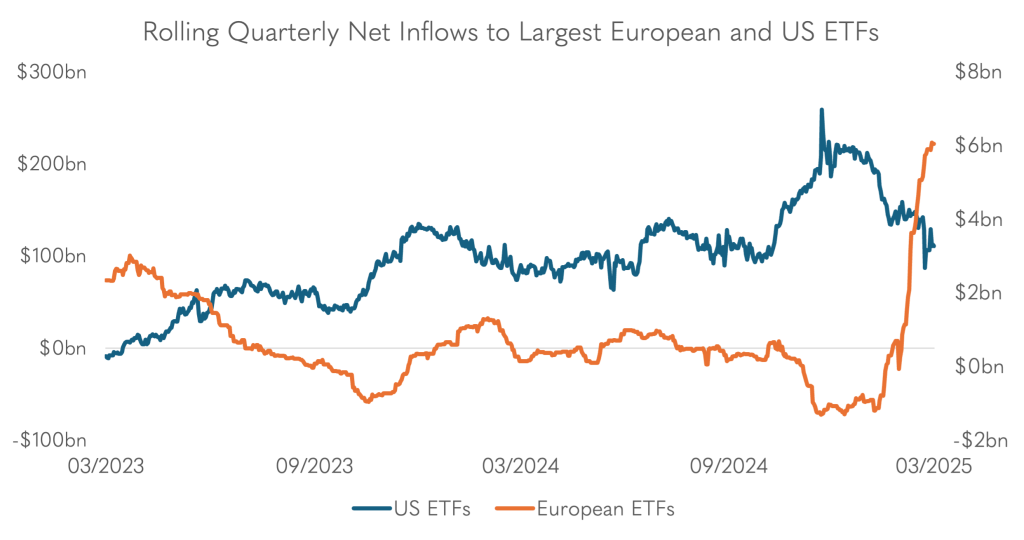

American assets have been under the spotlight recently, specifically equities which have whipsawed after each public comment made by President Donald Trump. The Volatility Index (VIX), which represents the expected annual volatility of the S&P 500 index, surged almost 70% from the end of January to its peak level on the 11th of March. This follows uncertainty in the markets primarily induced by geopolitics and tariffs. Investors have taken note and adjusted accordingly, with exponential allocations to European-themed Exchange-Traded Funds (ETFs), with the opposite trend seen in American-themed ETFs.

Source: High Street via Bloomberg (27 March 2025)

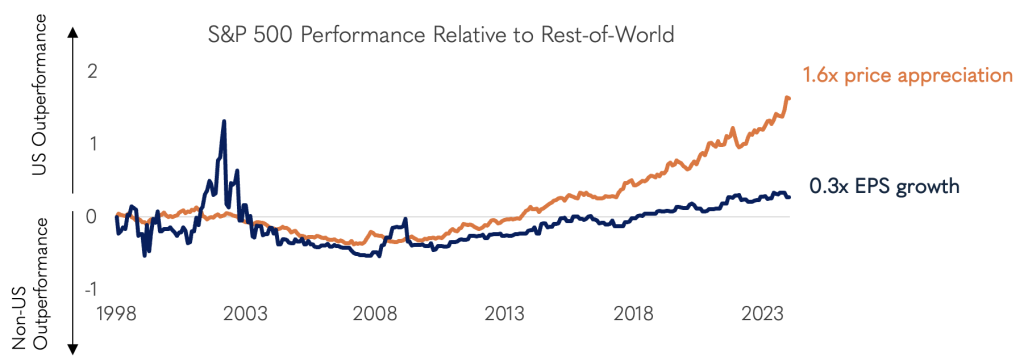

Recent global equity performance has been largely driven by the US. The chart below illustrates the US equity market performance relative to the rest of the world.

Source: High Street via Bloomberg (31 December 2024)

The orange line represents America’s share price dominance. Since the global financial crisis of 2008, the S&P 500 outperformed the rest of the world by nearly 200%. The blue line represents the relative earnings per share growth between the two regions. While the US has outpaced the rest of the world by approximately 70%, it is still 130% less than its price outperformance. As a result, valuation gains have been primarily responsible for this outperformance.

High Street believes a premium is justified owing to the strong cash generating ability and the depth of innovation within these companies. However, the valuation disconnect is too wide and implies that US earnings would have to outgrow the rest of the world by approximately 5% – 10% per annum over the next five years to justify its current premium. We have been actively reducing a portion of our US exposure in favour of non-US alternatives. While we believe that the American market is likely to retain its strong market leadership over time, there is opportunity to benefit from a valuation uplift in the rest of the world.